- Iowa dentist disciplined for unsanitary practice conditions

- ADA honors 10 new dentists for excellence in field

- Orthodontist pay vs. cost of living by state

- Oral surgeon pay vs. cost of living by state

- Wildfire smoke strafes Midwest, Northeast: 6 things healthcare leaders should know

- 9 pharmacy groups warn revised ACIP charter could delay vaccine access: 6 notes

- Private equity’s legal playbook for physician practices

- The outpatient orthopedic model built around doing less

- Where ASCs can find cost savings after the easy wins are gone

- NYU Langone grows South Florida presence with 2 practices

- The hidden cost of the GLP-1 boom: 5 notes

- ‘Hospitals without an outpatient footprint will struggle’: Health systems race to build ASC networks

- ‘Hospitals without an outpatient footprint will struggle’: Health systems race to build ASC networks

- Montefiore leader joins Northwell hospital as CNO, VP of patient care services

- Bad debt, charity care surge continues to squeeze hospitals

- 3 cardiology societies urge CMS to update TAVR coverage rules: 5 priorities

- UCSF nurses, physicians protest ED ‘boarding crisis’

- Inova’s next clinical chief keeps a fish pillow in her office

- Missouri outlaws insurance time limits on anesthesia: 5 things to know

- Texas hospital temporarily closes due to flooding

- Trump’s CDC Nominee Praises Vaccines, Without Vowing Independence From Kennedy

- Why ASCs should be watching the Medicare Advantage exodus

- LightForce Orthodontics appoints new CEO

- 39 behavioral health executive moves to know

- Good news for anesthesia

- MAX Surgical Specialty Management selects Sensei Cloud as enterprise practice management system

- Why some ASCs ‘are going to be left out’ of healthcare’s next era

- Median pay for anesthesiologists reaches $391K: Breakdown by state

- Is dental school becoming unattainable? 6 dentists weigh in

- Peak Dental Services becomes 1st DSO to deploy clinician well-being framework

- Aspen Dental continues expansion with South Carolina practice

- Texas safety net behavioral health provider projects $15M shortfall

- 4 dental deals totaling $308M

- Huahai poaches quality chief from Hengrui amid FDA manufacturing citations

- 24 new behavioral health study findings to know

- Maryhaven CEO steps down amid financial concerns

- GE HealthCare, Catholic Health strike 10-year, $500M technology partnership

- Thriveworks launches insight dashboard for referring providers

- What’s driving Arizona’s drug death surge? 6 things to know

- CMS proposal to block third-party vendors will upend remote monitoring services, health tech leaders say

- FDA Clears First Cholesterol Pill, Lipfendra, To Rival Costly Injections

- Statement on Regulation E-Delivery

- Paper Taper: Statement on Proposed Regulation E-Delivery

- Statement on Proposed Regulation E-Delivery

- One Of The Largest Epidural Studies Ever Delivers Reassuring News For Parents

- Bipartisan Senate bill seeks to build vigilance around foreign companies making drugs in US

- Coalition for Health AI launches implementation initiative for public health agencies

- Vanda shifts Nereus marketing into high gear with Schumacher IndyCar sponsorship

- Could A Vaccine Prevent Pancreatic Cancer In Those At High Risk?

- Heatwaves During Pregnancy Could Affect Baby's Brain Development, Study Suggests

- Brain 'Microstimulation' Works Long-Term To Restore Sense Of Touch After Spinal Cord Injury

- Otters, bears and Pharma Lions: inside Gilead’s bronze-winning Cannes spot

- 'Night Owls' At Risk Of Wider Waistlines, Unhealthy Hearts

- Facing Funding Losses, States Call Out Big Businesses With Employees On Medicaid

- Listen to the Latest ‘KFF Health News Minute’

- A Sales Tax on Doctor Visits and Medicine? In Missouri, Some Worry

- Readers Share Personal Insights on Deadly Denials and Pregnancy Centers

- Merck scores at FDA as Lipfendra becomes world's first oral PCSK9 treatment

- UnitedHealth Group to maintain 'restless' even after topping investor's Q2 expectations, CEO says

- 6 weeks into California’s psychiatric staffing mandate: What hospital leaders should know

- The best opportunities to expand behavioral healthcare access

- PsychPlus acquires Koa Health to scale mental health platform

- Senate HELP committee grills CDC nominee Erica Schwartz on vaccine policy, resistance to political interference

- 2 states join in expanding psychologist prescribing authority

- Ohio behavioral health clinic owners indicted in $9.3M Medicaid fraud case

- Bipartisan House bill tying doc pay to inflation earns resounding applause from providers

- West Tennessee Healthcare expands critical care support through eICU Program in partnership with Philips and hellocare.ai

- Sanofi opens new chapters in Pfizer, Moderna mRNA patent litigation sagas

- Novo gains head start on Lilly with European Commission approval of Wegovy pill

- Merck touts Keytruda front-line win in endometrial cancer subtype, marking a PD-1 first

- Wildfire Smoke Puts Millions At Risk Across Midwest, Northeast

- Lark Health, Samsung team up on AI-powered health coach for U.S. seniors

- 340B drug purchases hit at least $100B in 2025, administrator reports

- Buzzy Veradermics shows its oral minoxidil can tackle female pattern hair loss, too

- No patent protection for Stelara? No problem for J&J as Tremfya fills the void

- Amazon Pharmacy partners with eNavvi to provide real-time medication pricing, delivery info to providers

- Are Microplastics Linked To Higher Heart Attack Risk?

- Impulsivity In Third Grade Could Point To Future Struggles

- AI Can Create 'Ghosts' Of Lost Loved Ones, But Would You Want To Meet Them?

- Blood Test May Predict Alzheimer's Risk Up To 10 Years Before Symptoms Begin

- Kelun scores sac-TMT win in first-line NSCLC population missing from Merck’s massive phase 3 program

- OpenAI’s health AI chief: ‘Bet on the models getting better’

- Knee Pain? Ragged Cartilage? Research Suggests Surgery's Not The Best Answer

- THC/CBD Combo Might Ease Agitation In Late-Stage Dementia

- Facing Funding Losses, States Call Out Big Businesses With Employees on Medicaid

- Full-body scan startup Neko Health scores $700M to break into the U.S. market

- Elevance Health leaves D.C. Medicaid market, mulls future exits

- Sanofi teams up with Special Olympics Unified Football World, raises respiratory health awareness

- Insilico signs on with CDMO Bora in $2.5B AI drug discovery deal

- CMS proposes major Medicare reforms to shift physician pay, phase out MIPS and expand ACO participation

- Judi Health rebrands PBM arm as Judi Rx, unveils Judi Care unit

- With FDA approval for its breast cancer blockbuster hopeful, Celcuity could ‘belong in the hands’ of a Big Pharma

- Anthropic bets bigger on healthcare with Optum tie-up, UST integration

- FTC, CVS unveil settlement in ongoing insulin pricing case

- HHS promises its final rule barring pediatric gender care providers from Medicare is still coming

- AMA interoperability initiative brings structured clinical terminology to CPT codes

- Director's Note on What to Expect at the 2026 Partnerships with Sites Summit

- Lettuce Suspected In Growing Multistate Cyclospora Outbreak

- Startup Sonata launches preventive healthcare membership, linking clinical decisions with AI

- Why Are Family Doctors Leaving The Workforce? Retirement, Burnout Creating A U.S. Primary Care 'Brain Drain'

- Huyabio scores with Opdivo combo in 'milestone' skin cancer trial

- Unruly Patients Are Stressing ER Staff, Undermining Care

- Heatwaves Raise Hospital Admissions For Mental Health Woes

- Pain Patients Should Taper Opioids At Their Own Pace, Study Suggests

- U.S. Gun Suicides Hit Record High, Even As Firearm Deaths Decline Overall

- AstraZeneca pays up to $1.5B for EGFR lung cancer drug Zegfrovy from its spinoff Dizal

- Worried About Your Aging Parents? Welcome To The Caregiving Club

- Lawmakers Look To Make Abortion Shield Laws Less Dependent on Who’s Governor

- Knee Pain? Ragged Cartilage? Research Suggests Surgery’s Not the Best Answer

- Real Chemistry builds body of AI healthcare commercialization tools with Anatomi launch

- Inside agency view: Havas SO on authenticity, connection and pushing back against the ‘sea of sameness’

- Cellares' recent automated cell therapy wins have 'opened the biotech floodgates'

- Insulet, Calm join forces for diabetes care offerings with ‘Mind in Range’ wellness tools

- Remarks before the American-Hellenic Chamber of Commerce

- What Is An Aortic Dissection? The Condition That Killed Sen. Lindsey Graham

- Weight-Loss Drugs Help, But Exercise Is Still The Key To A Healthier Heart

- FDA's latest onshoring move homes in on streamlined facility registration, foreign plant scrutiny

- GSK to seek FDA approval for Jemperli in small but high-profile cancer use after phase 2 win

- Smartphones Can Increase Seniors' Risk Of Depression

- Pro Soccer Players Show Signs Of Shrinking Brains

- Adderall Misuse Falls Sharply Among Young Adults, Study Finds

- New KFF Poll Reveals Who Is Most Likely To Endorse Vaccine Myths

- A New Option For Long-Term Care Costs

- As GOP Cries Fraud, Newsom Backs Medicaid Spending on Housing and Food

- Lupin recalls more than 2.5M prescription eye drop bottles, citing possible contamination

- Journalists Discuss Raw-Milk Marketing, Extreme Heat, Opioid Settlement Spending

- Katie Couric's Memory Loss Scare Puts Rare Brain Condition In Spotlight

- Mild COVID Can Lead To Long-Term Hidden Eye Problems

- LGBTQ+ People Less Likely To Be Screened For Some Common Cancers

- Smartphone App Uses Voice To Predict Asthma, COPD Flare-Ups

- Seniors Know How Sharp They Are At Any Given Time, Study Finds

- Patients Face A Thicket of Red Tape Trying To Maintain Consistent Health Coverage

- AI Can Detect Previously Invisible MS Scars In The Brain

- A New Option for Long-Term Care Costs

- Remarks at the Society for Corporate Governance Conference

- GLP-1 Use Hits Record High As Medicare Opens Access To Weight-Loss Drugs

- Foundation Fights Medical Errors That Claim 200,000 U.S. Lives A Year

- New, Highly Accurate Brush Test Can Detect Mouth Cancer Within An Hour

- Innovative Hip Replacement Cuts Post-Surgery Risk Of Dislocation By 70%

- Global Study Finds Kids Worldwide Skipping Fruits And Vegetables

- Zimmer Biomet to Hire 500 in India as New Bengaluru Technology Centre Drives AI and MedTech Innovation

- AdaptHealth Investigates Data Breach After Social Engineering Attack, Possible Link to ShinyHunters Emerges

- Statement on the 2026 Regulatory Agenda

- Applying Agentic AI to Healthcare Delivery: The Key to True Transformation

- From Compliance to Clinical Action: Fixing the Broken Loop in Post-Market Surveillance

- SCAN Health Plan, Alignment Healthcare sue to challenge CMS' MA star ratings recalculations

- Regulatory tracker: Eisai, Biogen scoop up subQ Leqembi starter dose nod

- Remarks at the Economic Club of New York

- Is Your Organization Ready to Govern AI in Regulatory Affairs?

- CMS Proposes TAVR Medicare Coverage is Potential Boost for Edwards Lifesciences

Michigan healthcare freedom community forum

The Bureau of Labor Statistics (BLS) has been peddling the fiction that health insurance costs have been declining since the onset of COVID-19. This fiction has warped the entire Consumer Price Index, the most followed gauge of inflation in our economy. Inflation is running several percent higher than reported in the CPI due to several creative BLS fictions. Using the pre corruption methodologies of the 1970's, actual CPI is at least double that reported by BLS.

BLS will make minor changes to their calculation of the health insurance cost index in tomorrow's CPI report because absolutely no one believed their lies about health insurance costs. The new calculation will show sub 1% monthly increases in health care insurance costs. Still a lie, just a less egregious lie:

Health Insurance Is About To Boost Inflation After Months Of Relief

Molly Smith • November 13, 2023A change in how the government estimates health insurance costs is expected to give a slight boost to a popular US inflation measure, reversing a trend that had been providing some relief in recent months.

Beginning with Tuesday’s release of the October consumer price index, the Bureau of Labor Statistics will roll out a few changes to how it tabulates the category. In addition to a routine change in source data, the new methodology will aim to smooth some of the volatility and reduce time lags in the index.

After being a reliable drag on overall inflation for the past year, the new computation is widely anticipated to put upward pressure on the headline CPI, at least in the near term. It’ll also boost a narrower subset of services inflation that excludes energy and housing.

The Federal Reserve monitors so-called core services closely, but computes it based on separate price index figures within the personal consumption expenditures and income report.

“We think the Federal Reserve will continue to look past these shifts in health insurance CPI, as these estimates do not factor into the construction of the PCE price index, the Fed’s preferred inflation gauge,” Barclays Plc economists led by Pooja Sriram said in a report. That metric “is much more comprehensive than the retained-earnings concept used in the CPI,” they said.

Since health insurance policies and premiums vary widely, the BLS computes the cost through an indirect method. Essentially, it reflects the business cost of offering consumers health insurance, whereas services for seeing a doctor or a hospital stay are calculated separately and are at or near record-high price levels.

The health insurance index, by contrast, is currently at its lowest reading in nearly six years. But what Americans actually pay for coverage is a different story.

US employers expect the total benefit cost per employee to rise 5.4% on average next year — even after they make changes to their plans to slow cost growth — according to a preliminary survey from workplace consultant Mercer. Other polls have found that nearly 40% of Americans have had to forgo healthcare because they couldn’t afford it.

The CPI index of health insurance measures what customers pay into their policy that’s not distributed out in benefits — also known as an insurer’s retained earnings, or profit margins. The BLS currently receives this data annually, but is switching to a semiannual update to reduce lags in the index.

For the past year, the health insurance category has fallen at a roughly 4% clip each month. Bloomberg Economics and Bank of America Corp. expect the changes to result in CPI health insurance rising roughly 1% starting in the October report. Barclays sees that pace lasting through March 2024 once the BLS incorporates the semiannual data, while Goldman Sachs Group Inc. expects the category to slow to a flat reading by April.

The BLS doublespeak on their health care index 'improvements':

https://www.bls.gov/cpi/additional-resources/improvements-cpi-health-insurance-index.htm

Improvements to the CPI Health Insurance Index

CORRECTION TO THIS PAGE MADE AUGUST 23, 2023

When this webpage was first published on 08/22/2023 the equation for the TTM sequential relative was incorrectly shown as a duplicate of the equation for the TTM retained earnings ratio.

Introduction

BLS will implement changes to the Consumer Price Index (CPI) health insurance methodology starting with the calculation of October 2023 indexes. The pre-October 2023 method is based on an annual calculation using aggregated health insurance premium and benefit data. Two concerns with the pre-October 2023 methodology are the volatility in the annual data and the lag involved in incorporating the health insurance financial data. To address these concerns, we are introducing smoothing to the index to reduce the volatility. We will also incorporate semiannual financial data, which reduces the lag in the index.

After providing an overview of the health insurance data and pre-October 2023 methodology, we discuss the recommendations that led to the changes in the methodology. Then, we discuss the new methodology that uses a smoothed semiannual index instead of an unsmoothed annual index. Finally, there are issues relating to the transition which require adjustments to correct.

CPI health insurance methodology

The CPI measures health insurance inflation using an indirect method.[1] The indirect method views health insurance as a composite good. Total premiums pay for insurance services (risk protection, claim processing, etc.) and medical goods and services through the insurer reimbursements to providers. Rather than pricing the full premium of health insurance plans, the CPI prices the services provided by the health insurer measured by the portion of the total premium that isn’t used to indirectly purchase medical goods and services. The premiums minus benefits spending is known as the retained earnings.

Then, the measured prices of medical goods and non-insurance services (e.g., physicians, hospitals, etc.) are defined to be the total reimbursed amount and include any payments from insurers. The associated out of pocket expenditure weights are reassigned from premiums to the medical goods and non-insurance services categories. So, the only weight remaining to the health insurance index reflects the retained earnings.[2] Since the insurance spending on medical benefits is included in the non-insurance medical indexes, the insurance services price should not include the impact of benefit inflation on total premiums. Instead, BLS defines the price of these insurance services as the ratio of retained earnings (premiums minus benefits) and real benefits (benefits adjusted for medical inflation).

Prior to October 2023, the health insurance premium and benefits data used in the calculation of the health insurance price relative are annual. The CPI health insurance monthly relative is the twelfth root of the year over year change in the retained earnings to benefit ratio times medical benefits inflation. There are two retained earnings relatives. The first covers most health plans and reflects most of the weight of the index. The second covers plans not included in the first calculation, specifically long-term care (LTC) insurance and Medicare Part D.

Despite some practical advantages of the indirect method, there are some limitations. First, the retained earnings ratio can be volatile, which can cause the retained earnings relative to fluctuate substantially from one year to the next. The reason for this volatility is that insurance plans cover a full year, so premiums are only updated once a year, and utilization within the year can be unpredictable. If utilization is unexpectedly high in a given year, the retained earnings to benefits ratio will fall. The next year, insurers will raise premiums to rebuild their reserves, and the retained earnings to benefits ratio will rise.

Another limitation is that the data are lagged. The health insurance index does not reflect contemporaneous retained earnings information since there is a lag in the availability of the retained earnings data to the CPI. The primary data source for the retained earnings relative in the CPI health insurance index is the U.S. Health Insurance Industry Analysis Report published by the National Association of Insurance Commissioners (NAIC) on an annual basis. The main health insurance relative combines this data with data from California as managed care plans in California report to a different regulator. The second retained earnings relative that covers long term care (LTC) and Medicare part D uses data from the NAIC Accident and Health Policy Experience Report.

CNSTAT report and recommendations

The BLS recently asked the National Academies of Science, Engineering, and Medicine, Committee on National Statistics (CNSTAT) for recommendations on improving the CPI, including recommendations on pricing health insurance. The final CNSTAT report was released in 2022.[3] CNSTAT recommended that the BLS continue to use the indirect method for pricing health insurance (recommendation 5.1) but made several recommendations for how the indirect method could be improved.

Smoothing

One issue with the pre-October 2023 method is there can be a lot of volatility in the retained earnings data from one year to the next. There is a question as to whether smoothing the retained earnings data using a moving average is desirable when calculating the relative. This section discusses the arguments for and against smoothing the annual retained earnings data.

The argument against smoothing is that the volatility represents real price changes that should be reflected in the index. If consumers on average have unexpectedly high utilization in a given year, they are receiving a benefit from having their premium locked in for the year. In terms of the insurance services, they are paying less for them (lower retained earnings) and getting more out of them (assuming the quantity of insurance services is proportional to utilization), which means that the price of insurance services has fallen. If this is considered a real price change, then it is irrelevant that it will likely be reversed in the following year. It can be viewed analogously to a sale, with consumers benefitting from prices that are lowered temporarily.

The argument for smoothing is that the relevant price when considering insurance is the ex-ante price.[4] Any ex-post deviations from expected utilization should not be considered real price changes. Individuals can be viewed as facing a fixed price schedule with uncertain utilization. The actual realized retained earnings to benefits ratio will depend on utilization and can show a change in price even if the price schedule is fixed. In similar situations where the price depends on total utilization, the CPI will hold utilization constant when pricing (for example, in the pricing of electricity). CNSTAT argued that the ex-ante price is the relevant price and suggested we consider smoothing (recommendation 5.3). We agree with CNSTAT that the ex-ante price is the more appropriate measure, so a relative calculated from smoothed retained earnings data will be a more accurate measure of price change. A limitation of smoothing is that if the retained earnings to benefit ratio changes for ex-ante reasons (reflecting a real ex-ante price change), smoothing will delay the impact of this change on the price index.

Incorporating retained earnings data sooner

Pre-October 2023, the annual retained earnings data is incorporated into the CPI starting in October after the calendar year for the retained earnings data. For example, in October 2022, retained earnings data was first incorporated into the index reflecting the change in the retained earnings to benefits ratio from 2020 to 2021. This annual change is smoothed over 12 months, so the 2021 retained earnings data will not be fully reflected in the index until September 2023.

Exploring the use of quarterly data to improve the timeliness of the index was another recommendation of the CNSTAT panel (recommendation 5.6).

Proposed changes to the CPI health insurance index

After conducting extensive research on these recommendations, we determined that the health insurance index could be improved by smoothing the retained earnings data and by using more timely, higher frequency data. In this section, we summarize how we plan to implement these changes to the methodology.

Smoothing the Retained Earnings Data

Following the recommendation to smooth the retained earnings data, we investigated different window lengths for the moving average and considered simple versus exponential moving averages. Ultimately, we chose to smooth using a 2-year simple moving average of the retained earnings ratio. Unusual deviations in the retained earnings are generally reversed the following year, so a 2-year average is sufficient for smoothing. Using additional years has less of an impact on smoothing and introduces unnecessary lag. We also favor using a simple moving average versus an exponential moving average as the exponential moving average will retain more of these 1-year deviations. The smoothing will be applied to both retained earnings calculations.

Semiannual updates

Overall, semiannual and quarterly updates are feasible and improve the timeliness of the index (by six months for semiannual updates and nine months for quarterly updates). A limitation of the quarterly updates is that the data is not provided at the level of detail that allows us to exclude out-of-scope plans. So out-of-scope plans are included in the calculation to impute quarterly changes in the in-scope retained earnings. The quarterly updating can increase volatility, and there is no way to know whether this volatility is driven by in-scope plans (reflecting a true price change that we would want to show in the index) or out-of-scope plans.

Updating twice a year is a clear improvement over the annual method and improves the timeliness of the index by six months compared to the annual updates. The additional benefit of improved timeliness (3 months) of updating quarterly is offset by an increase in volatility. At this time, we decided to switch to semiannual updates as it is not clear the added timeliness of updating quarterly is worth the increase in volatility. However, we will continue to research quarterly data and may incorporate it in the indexes at some point in the future. The semiannual updates will apply to the main retained earnings calculation. The second retained earnings calculation, covering LTC and Medicare part D, will continue to update annually in October, though we will continue to explore options for imputing the semiannual changes for this data.

Computation of semiannual updates

In terms of implementing the semiannual updates, the mid-year report includes data through June 30, and the final report includes the full year data. To calculate the 2nd half data, we subtract the mid-year report values from the full year data. Once we have the data by half, there are several options for creating semiannual relatives. The formula we chose to incorporate the semiannual updates is a sequential trailing 12 month relative of the retained earnings to benefit ratio. One issue is that the NAIC data are not complete and must be supplemented with data from managed care plans in California that report to a different regulator. The California data are not available at the necessary level of detail semiannually, so we impute the first half of California data using changes in the NAIC data.

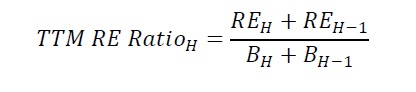

The trailing 12 month (TTM) index pools two halves of data and calculates the sequential relative. Once the second half of the year data is incorporated, the TTM and full year indexes will be identical. This is a desirable property of the TTM index as it will equal the full year index once each index incorporates the same data. For this reason, the TTM index is our preferred method as it will automatically correct any errors in the first half data, whether due to data reporting issues or imputation error relating to the California data. The main advantage of the semiannual index is that it will incorporate this change six months sooner than the annual index. The TTM retained earnings to benefit ratio in half H is:

The TTM sequential relative is:

Incorporating both changes, the TTM smoothed relative in half H is:

This is a semiannual relative, so the monthly retained earnings relative is calculated by taking the sixth root. The monthly retained earnings relative is:

The monthly retained earnings relative is multiplied by the relatives for medical benefits to form the health insurance relative. This is the calculation for the semiannual updates starting in April 2024 that will incorporate the first half of 2023 data. To switch from an unsmoothed annual index to a smoothed semiannual index, adjustments must be made to the October 2023 update that incorporates the 2022 annual data. We discuss the adjustments for this transition period in the next section.

Transition

Both methodological changes (smoothing retained earnings and incorporating retained earnings data sooner) introduce issues with the transition from pre-October 2023 methods. The first issue relates to the timing of the semiannual and annual indexes. Since, the semiannual index is six months ahead of the annual index, switching from annual to semiannual requires speeding up the next annual update. Instead of spreading the 2022 annual update over 12 months, it would be spread over six months by taking the sixth root instead of the twelfth root. Then, in April 2024, we would be able to update the indexes with 2023 first half retained earnings data since the 2022 data will be fully reflected in the index.

The second issue is that, unless a correction term is applied, switching from an unsmoothed to a smoothed relative will create a permanent distortion in the index. See the technical appendix on smoothing retained earnings for an example that illustrates how this distortion arises and how we derive the corrected relative.

Summary

Following recommendations from CNSTAT, starting in April 2024, we will switch the retained earnings calculation from an annual relative updated in October to a two year moving average using semiannual data and will update in April and October.[5] The next annual update in October 2023 will involve a six month transition to account for issues relating to changing in methodology. Table 1 provides a summary of the update timing moving forward.

Table 1: Summary of future updates to the CPI health insurance index Index Month Summary of update October 2023

Incorporate 2022 annual retained earnings data as an adjusted smoothed relative. For the main RE calculation, this update will be spread over six months. For the LTC/Part D calculation, it will be spread over a year. See the technical appendix for the derivation of the adjustment term. April 2024

Update the main RE calculation to incorporate the first half data for 2023. The update will be the semiannual sequential smoothed relative and smoothed over six months. The contribution of California managed care plans to the first half of 2023 retained earnings and benefits will be imputed from changes in the NAIC data. October 2024

Annual update to incorporate full year 2023 data. Second half of 2023 values are calculated by subtracting the first half totals (or first half imputed values for CA managed care plans). For the main RE calculation, the second half data is incorporated as the semiannual sequential TTM smoothed relative and smoothed over the following six months. For the LTC/part D retained earnings calculation, full year 2023 values are incorporated as a smoothed annual relative which is spread over the following 12 months. April/October

In future years, the April/October update process will continue. First half data will be incorporated in April and the full year update will occur in October. Note: This is the tentative schedule for the proposed methodology changes. BLS may amend this schedule in the future as we learn from experience.

Details regarding the transition to this new methodology are provided in: Technical Appendix to Improvements to the CPI Health Insurance Index: Transitioning from an unsmoothed to a smoothed relative

Last Modified Date: August 30, 2023

[1] For more detail on the CPI health insurance methodology see the CPI medical care factsheet.

[2] An alternative to the indirect method would be to price total premiums. Then, the prices and weights of medical goods and non-insurance services would only include out of pocket payments.

[3] The final report can be found here. Chapter 5 focuses on improvements to the medical indexes, with particular emphasis on the pricing of health insurance.

[4] The ex-ante price refers to the insurers setting premiums before knowing what the utilization will be during year. The premium is set based on expected utilization. The benefits spending we observe is based on actual utilization (ex-post), which may differ from what the insurance company expected when setting the premium.

[5] Part of the index will still use annual data but will also switch to using a two year moving average.

The BLS October 2023 CPI report is now available:

https://www.bls.gov/news.release/pdf/cpi.pdf

Go to its Table 2, Page 15 and scroll down to Medical care services. BLS claims the costs of Medical care services declined by 2% from October 2022 to October 2023. BLS claims the costs of Health insurance, the bottom item in the Medical care services section, declined by 34% from October 2022 to October 2023.

Get MHF Insights

News and tips for your healthcare freedom.

We never spam you. One-step unsubscribe.

Sponsors

J & DE Family Charitable Fund

Friends

of MHF

Kelly Grotendiek

Philip Harbach

Dale Johnson

Drs. Jeffrey and Joni Jones

Vickie Kahle

Tammy Kipen

Marlin & Kathy Klumpp

Melanie Kurdys

Ruth Nobel

Patrick Peterson

Stephanie Poortenga

Jeanne Smit

Ben and Hope Staal

John Tuinstra

Jacki VanHuis

Sandy Walker

Sign Up for MHF Insights to keep up on the latest in Michigan Health Policy