Everyone on Medicaid either is a responsible adult, or has a responsible adult to make their healthcare decisions. So why are we paying thousands of middlemen to complicate their care?

Medicaid Middlemen

MDHHS case managers, contracted managed care insurance plans, and other bureaucratic gatekeepers absorb billions of tax dollars that could pay directly for care. Michigan Medicaid is arguably the most out-of-control, expensive part of the state budget.

In addition, it imposes an incalculable burden of time and suffering on patients and clinicians with its byzantine billing and records system.

Michigan should convert Medicaid and Healthy Michigan plans to expanded HSAs based on need.

Updated Health Savings Accounts

Health Savings Accounts (HSAs) are better than ever for individual care, now that they can pay Direct Primary Care (DPC) memberships.

Michigan physicians are bailing out of corporate healthcare to become independent. I hear there’s a new DPC conversion in Traverse City, and a multi-practice group is spreading across the Mitten.

Cash is the universal medium to access services. Such simplicity is mind-boggling, especially compared to our complicated Medicaid.

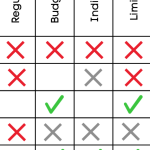

Process basics to consider

- Obtain a federal Medicaid HSA waiver.

Approval for a traditional waiver like Indiana’s would be relatively simple. However, I’d aim higher: an expanded HSA to allow no-cap deposits. Since this empowers individuals with greater independence, and streamlines the state role, I suspect CMS would be agreeable. - Verify participant qualifications to maximize funds for the truly needy.

This is an existing MDHHS function. It shouldn’t be difficult since COVID exemptions have been repealed. - Fund HSAs for all qualified Medicaid participants.

Several methods come to mind. I’m sure others can think of more features.- Plan at least two funding levels: chronic disability and temporary need.

It may seem necessary to gauge need from prior medical records, but that will get complicated very rapidly. - Pre-fund with installments monthly or bi-annually.

- Match all patient contributions.

- Plan for the recipient to have full ownership of the account.

- Plan at least two funding levels: chronic disability and temporary need.

- Transition insurance to back-up only. No managed care, no prior authorization, no access to patient records except for catastrophic claims.

- Redundant state employees may retire early or enter the private sector workforce.

Objections

There will be fraud!

Banks and the IRS provide tight guardrails for HSAs.

And let’s not forget that today’s Medicaid is rife with waste, fraud and abuse. This move is a much-needed reset.

Until now, middleman billing covered a multitude of sins. With middlemen gone, and an HSA bank card paying for service, transparency is a breeze.

The Medicaid population can’t handle HSAs!

Let’s be nice, here, shall we? New HSA card-holders will have a learning curve. Especially, perhaps, generational Medicaid families. And that’s OK.

People new to HSAs will network their communities and social media, ask their doctors, ask the bank holding the HSA.

Forging new bonds outside the official welfare system is healthy. Shopping is an innate human urge. Local, sustainable connections help grow personal independence and responsibility.

And the churn population will take to an HSA like a duck to water. Families of disabled children, especially, know what they need and often where to find it. Until the HSA, their primary difficulty was finding an appointment and getting permission for Medicaid to pay for it.

We have to help them!

I predict lobbies will want to encumber a transition to Medicaid HSA with navigators, care managers, and others to hand-hold and collect data. (MDHHS in the lead, here.)

I’d recommend limiting transition to an information brochure, and no more from the state.

This is less harsh than it sounds. Letting people shop for their own care will release their economic voice and a wave of pride at their budding self-preservation skills.

Imagine the boost to human dignity when, instead of trying to make an appointment with Medicaid, someone can say, “I have an HSA.”