- GI is exploding with new tech—but how do patients feel about it?

- HHS, CMS form healthcare advisory committee

- NewYork-Presbyterian named in antitrust lawsuit

- Maryland physician to pay $500K+ to settle false claims allegations

- FirstHealth breaks ground on $43M replacement hospital

- Rhode Island oral surgeon launches Congressional campaign

- Johns Hopkins affiliate names new CEO

- 6 things to know about the pharmacy technician workforce

- FDA adds seizure warning to CSL flu vaccine label

- Premier Anesthesia, City of Hope Phoenix ink partnership

- 20 behavioral health leaders challenge industry assumptions

- Why an $8B health system recommitted to its original name

- What simulation training revealed about GI skills gaps

- Judge dismisses physician’s wrongful termination suit against staffing firm

- 3 California behavioral health centers to close amid funding shifts

- Missouri system taps CFO as COO

- HCA moves to block disclosure of physician, patient outcomes post-hospital acquisition

- 6 things to know about CMS’ GLP-1 pilot model: KFF

- North Carolina practice to close after 40+ years

- St. Tammany opens outpatient cardiology center

- Indiana bars autism therapy provider from Medicaid billing: Wall Street Journal

- 6 dental practice openings to know

- APRNs, PAs account for most antipsychotic prescriptions for Medicare Part D: Study

- What will surprise ASC leaders about spine in 5 years?

- Why culture is the secret to a high-performing ASC

- Oklahoma House passes bill expanding scope of dental assistants

- Dr. Nellie Kim-Weroha joins American Association of Orthodontists’ Board of Trustees

- California behavioral health agency to close 2 centers

- Cardiologist named chief medical officer of biotech company

- St. Luke’s CFO joins RCM company’s advisory board

- 52 DSOs to know: 2026

- 10 hospitals, health systems looking for CFOs

- 10 health system rating downgrades

- FDA Warns Biotech Firm Over Cancer Drug Anktiva Claims

- Bees and Hummingbirds May Be Consuming Small Amounts of Alcohol

- Two States Sue Cord Blood Company Over Misleading Claims

- North Star’s restructuring moves forward

- Illinois hospital pauses patient care amid payroll challenges

- What the Best-Performing Revenue Cycles Have in Common

- New WHO Guidance Aims To Speed Tuberculosis Testing

- As questions swirl around ATTR competition, Alnylam plots path to market leadership for Amvuttra

- Outspoken ACIP member steps down amid vaccine panel uncertainty: reports

- Egg-based drugmaker Neion Bio emerges from stealth to cook up multi-product biosimilar collab

- Genentech walks the walk in lupus as sponsor of annual awareness and fundraising event

- Study Reveals How Many Americans Consider Using a Gun

- Massive Study Finds Stress and Grief Don’t Cause Cancer

- Ultra-Processed Foods Harm Fertility In Both Men And Women, Studies Reveal

- Small Daily Habits Can Add Up To Better Heart Health

- Ritalin Might Protect ADHD Kids' Long-Term Mental Health, Study Finds

- Can You Drink Enough Fluids To Prevent Kidney Stones? Maybe Not, New Study Says

- Clasp, loan-linked hiring tool for employers, clinches $20M to expand amid federal loan caps

- Taking a GLP-1? Doctors Say Not To Forget About Movement and Mental Health

- OpenEvidence rolls out AI medical coding feature

- CDC’s Acting Chief Promises a Return to Stability in a Tumultuous Moment

- California peer-run behavioral health center to close amid funding shift

- Remarks at the Financial Stability Oversight Council Meeting

- ‘Integration only works if data lives in the same system’: How 5 systems are operationalizing behavioral health

- Medicaid work rules and enrollment losses: 6 notes

- Inside UHS’ playbook for responsible behavioral health growth

- Epic4 Specialty Partners adds Illinois practice

- Adventist Health cuts operating loss in 2025

- ‘Burning the candle from both ends’: New York hospital CFO on rising costs, revenue cuts

- The unsolved problems still plaguing dentistry

- American Dental Association adds mental health, GLP-1 prompts to patient forms

- 21 revenue cycle executive moves in 2026

- North Carolina orthodontic practice opens 7th location

- Virginia hospital boosts workplace safety reporting 245% with 3 strategic shifts

- ADA urges CMS to proceed with adult dental coverage expansion

- RWJF: Between 5M and 10M people could lose Medicaid coverage in 2028 under work requirements

- Imagen Dental Partners adds Washington practice

- How pharma marketers can capitalize on HCPs’ AI, social media and streaming habits

- Federal Officials Investigate States That Require Abortion Coverage

- Corcept's lead drug bounces back from FDA snub with different approval as Lifyorli in ovarian cancer

- Ionis slashes Tryngolza's price tag by 93% ahead of anticipated label expansion

- FDA approves Denali's Hunter syndrome drug, handing rare disease community a win

- Baby Walkers Sold on Amazon Recalled Over Fall Risk

- Want To Protect Your Brain? Science Says Exercise

- HelloFresh Pizza Recall Issued in 10 States Over Metal Risk

- Clinical Trials Have Too Much Data…That’s the Problem.

- Clinical Trials Have Too Much Data…That’s the Problem.

- CMS reveals new Medicaid model that supports coordination for children with complex needs

- Novartis sued by breast cancer patient over branded drug websites’ data-sharing practices

- Takeda targets $1.3B in cost savings in further restructuring

- Biogen pays $20M upfront to tap into Alteogen's subQ delivery tech

- 'Universal Donor' Blood Supplies Dangerously Low, Study Warns

- Why Stepping Outside May Help You Eat Better

- U.S. Medicine, Science Facing An Online Misinformation Siege, Poll Concludes

- Childhood Obesity Undercuts The American Dream For Some, Study Says

- Inclusive High Schools Benefit All Students, Not Just LGBTQ Teens

- Parental Loss Due to Drugs, Violence Raises Child Death Risk by 2,000%

- As Boehringer touts US launches, board chairman worries EU is 'falling further behind'

- The evolving state of exome and genome sequencing

- Demoralized CDC Workforce Reels From Year of Firings, Funding Cuts, and a Shooting

- An Arm and a Leg: Steep Health Care Costs Steer Americans to Tough Decisions

- Qualified Health locks in $125M in fresh funding to scale enterprise AI at health systems

- Misery Loves [Investment] Company?: Remarks at the 2026 Investment Company Institute Investment Management Conference

- Study: Nearly 1 in 5 pediatric hospital deaths involve sepsis

- Opening Remarks at the Digital Asset Summit 2026

- CVS Caremark, FTC reach settlement in insulin pricing case

- UCB unveils plan to build $2B biologics plant near its US headquarters in Atlanta

- PeaceHealth sued over plans to tap out-of-state staffer ApolloMD for Oregon EDs

- New Lyme Disease Vaccine Shows Strong Results in Trial

- TrumpRx Adds Diabetes, COPD Drugs at Steep Discounts

- Highmark reports $175M net loss for 2025 as financial headwinds batter health plan

- Listen to the Latest ‘KFF Health News Minute’

- Abivax hires commercial chief from Takeda to infuse Entyvio expertise into IBD launch prep

- ImmunityBio hit with FDA warning letter over Anktiva promotions in TV ad, podcast episode

- Alcohol Prep Pads Recalled Over Bacteria Risk, Cardinal Health Says

- Fewer patients traveled for abortions in 2025 as telehealth care increased, report finds

- Cologuard campaign reunites ‘Full House’ stars to give ‘The Talk’ about colon cancer screening

- Lilly to remove certain insulin products from European markets by 2027

- Karyopharm, looking to jump-start Xpovio, reports mixed results in myelofibrosis

- Study Warns Fluoride Bans May Raise Tooth Decay in Children

- WuXi Bio's record number of new projects in 2025 leaned heavily on US clients

- “Me engañaron”: agentes encadenan a un padre que había ido al ICE a reunirse con sus hijos

- Gilead inks Manta pact to dive deeper into cancer patient support

- Cheap Children's Clothing Tainted With Lead, Study Says

- Insulin Prices Fell For Medicare Patients Under Biden-Era Caps, Study Finds

- New Fathers Face Mental Health Challenges, Study Finds

- Your Choice Of Booze Influences Your Risk Of Death, Study Says

- AI Gets a 'D' When Judging Scientific, Medical Claims

- New Online Tool Helps Parkinson's Patients Weigh Brain Implant Decision

- AI chatbot use for health information up 16% from 2024: Rock Health survey

- ‘They Tricked Me’: A Father Was Chained After He Went to ICE To Reunite With His Kids

- Wilmington PharmaTech commits $50M to US API expansion

- Strides recalls nearly 90K bottles of children's ibuprofen after contamination complaints

- Trump administration unveils national policy framework for AI as it moves to override state laws

- Breast Cancer Locator System Submitted for De Novo 510(k) by Cairn Surgical

- Breast Cancer Locator System Submitted for De Novo 510(k) by Cairn Surgical

- 17 spine surgery firsts in Q1

- 17 spine surgery firsts in Q1

- Cencora acquiring EyeSouth Partners' retina business for $1.1B

- Aunque tengas seguro dental, la factura puede ser muy alta

- Massive class action seeking RICO penalties against Takeda, Lilly presses forward with SCOTUS order

- A look at how Optum Rx is using AI to address pharmacy fraud, waste and abuse

- Nursing Homes Accused of False Diagnoses To Hide Drug Use

- FDA Approves Higher-Dose Wegovy To Help People Lose More Weight

- Teens Often Pressured To Send Sexual Photos by Someone They Know, Study Finds

- CommonSpirit, Humana reach 3-year national network agreement

- Match Day 2026: Growth in emergency medicine, psychiatry

- Nearly 90,000 Bottles of Children’s Ibuprofen Recalled Nationwide

- FTC launches multi-bureau Healthcare Task Force to spot 'new priority areas for enforcement'

- Algunos adultos de mediana edad deciden posponer la atención médica hasta tener Medicare

- ¿Qué tan bajo se puede llegar? Las cambiantes guías para el control de la presión arterial

- Rural hospitals could apply for temporary interest-free construction, renovation loans under new bipartisan bill

- Rural Residents Have Highest Cancer Death Rates, Researchers Say

- Your Bank Account Might Show How Well Your Brain Will Age, Researchers Say

- Insurance Lapses Play Havoc With Diabetes Management, Study Shows

- Psychedelics Aren't Better Than Antidepressants In Treating Depression, Review Concludes

- A Nasal Swab for Alzheimer's? Duke Team Has One in Testing

The Bureau of Labor Statistics (BLS) has been peddling the fiction that health insurance costs have been declining since the onset of COVID-19. This fiction has warped the entire Consumer Price Index, the most followed gauge of inflation in our economy. Inflation is running several percent higher than reported in the CPI due to several creative BLS fictions. Using the pre corruption methodologies of the 1970's, actual CPI is at least double that reported by BLS.

BLS will make minor changes to their calculation of the health insurance cost index in tomorrow's CPI report because absolutely no one believed their lies about health insurance costs. The new calculation will show sub 1% monthly increases in health care insurance costs. Still a lie, just a less egregious lie:

Health Insurance Is About To Boost Inflation After Months Of Relief

Molly Smith • November 13, 2023A change in how the government estimates health insurance costs is expected to give a slight boost to a popular US inflation measure, reversing a trend that had been providing some relief in recent months.

Beginning with Tuesday’s release of the October consumer price index, the Bureau of Labor Statistics will roll out a few changes to how it tabulates the category. In addition to a routine change in source data, the new methodology will aim to smooth some of the volatility and reduce time lags in the index.

After being a reliable drag on overall inflation for the past year, the new computation is widely anticipated to put upward pressure on the headline CPI, at least in the near term. It’ll also boost a narrower subset of services inflation that excludes energy and housing.

The Federal Reserve monitors so-called core services closely, but computes it based on separate price index figures within the personal consumption expenditures and income report.

“We think the Federal Reserve will continue to look past these shifts in health insurance CPI, as these estimates do not factor into the construction of the PCE price index, the Fed’s preferred inflation gauge,” Barclays Plc economists led by Pooja Sriram said in a report. That metric “is much more comprehensive than the retained-earnings concept used in the CPI,” they said.

Since health insurance policies and premiums vary widely, the BLS computes the cost through an indirect method. Essentially, it reflects the business cost of offering consumers health insurance, whereas services for seeing a doctor or a hospital stay are calculated separately and are at or near record-high price levels.

The health insurance index, by contrast, is currently at its lowest reading in nearly six years. But what Americans actually pay for coverage is a different story.

US employers expect the total benefit cost per employee to rise 5.4% on average next year — even after they make changes to their plans to slow cost growth — according to a preliminary survey from workplace consultant Mercer. Other polls have found that nearly 40% of Americans have had to forgo healthcare because they couldn’t afford it.

The CPI index of health insurance measures what customers pay into their policy that’s not distributed out in benefits — also known as an insurer’s retained earnings, or profit margins. The BLS currently receives this data annually, but is switching to a semiannual update to reduce lags in the index.

For the past year, the health insurance category has fallen at a roughly 4% clip each month. Bloomberg Economics and Bank of America Corp. expect the changes to result in CPI health insurance rising roughly 1% starting in the October report. Barclays sees that pace lasting through March 2024 once the BLS incorporates the semiannual data, while Goldman Sachs Group Inc. expects the category to slow to a flat reading by April.

The BLS doublespeak on their health care index 'improvements':

https://www.bls.gov/cpi/additional-resources/improvements-cpi-health-insurance-index.htm

Improvements to the CPI Health Insurance Index

CORRECTION TO THIS PAGE MADE AUGUST 23, 2023

When this webpage was first published on 08/22/2023 the equation for the TTM sequential relative was incorrectly shown as a duplicate of the equation for the TTM retained earnings ratio.

Introduction

BLS will implement changes to the Consumer Price Index (CPI) health insurance methodology starting with the calculation of October 2023 indexes. The pre-October 2023 method is based on an annual calculation using aggregated health insurance premium and benefit data. Two concerns with the pre-October 2023 methodology are the volatility in the annual data and the lag involved in incorporating the health insurance financial data. To address these concerns, we are introducing smoothing to the index to reduce the volatility. We will also incorporate semiannual financial data, which reduces the lag in the index.

After providing an overview of the health insurance data and pre-October 2023 methodology, we discuss the recommendations that led to the changes in the methodology. Then, we discuss the new methodology that uses a smoothed semiannual index instead of an unsmoothed annual index. Finally, there are issues relating to the transition which require adjustments to correct.

CPI health insurance methodology

The CPI measures health insurance inflation using an indirect method.[1] The indirect method views health insurance as a composite good. Total premiums pay for insurance services (risk protection, claim processing, etc.) and medical goods and services through the insurer reimbursements to providers. Rather than pricing the full premium of health insurance plans, the CPI prices the services provided by the health insurer measured by the portion of the total premium that isn’t used to indirectly purchase medical goods and services. The premiums minus benefits spending is known as the retained earnings.

Then, the measured prices of medical goods and non-insurance services (e.g., physicians, hospitals, etc.) are defined to be the total reimbursed amount and include any payments from insurers. The associated out of pocket expenditure weights are reassigned from premiums to the medical goods and non-insurance services categories. So, the only weight remaining to the health insurance index reflects the retained earnings.[2] Since the insurance spending on medical benefits is included in the non-insurance medical indexes, the insurance services price should not include the impact of benefit inflation on total premiums. Instead, BLS defines the price of these insurance services as the ratio of retained earnings (premiums minus benefits) and real benefits (benefits adjusted for medical inflation).

Prior to October 2023, the health insurance premium and benefits data used in the calculation of the health insurance price relative are annual. The CPI health insurance monthly relative is the twelfth root of the year over year change in the retained earnings to benefit ratio times medical benefits inflation. There are two retained earnings relatives. The first covers most health plans and reflects most of the weight of the index. The second covers plans not included in the first calculation, specifically long-term care (LTC) insurance and Medicare Part D.

Despite some practical advantages of the indirect method, there are some limitations. First, the retained earnings ratio can be volatile, which can cause the retained earnings relative to fluctuate substantially from one year to the next. The reason for this volatility is that insurance plans cover a full year, so premiums are only updated once a year, and utilization within the year can be unpredictable. If utilization is unexpectedly high in a given year, the retained earnings to benefits ratio will fall. The next year, insurers will raise premiums to rebuild their reserves, and the retained earnings to benefits ratio will rise.

Another limitation is that the data are lagged. The health insurance index does not reflect contemporaneous retained earnings information since there is a lag in the availability of the retained earnings data to the CPI. The primary data source for the retained earnings relative in the CPI health insurance index is the U.S. Health Insurance Industry Analysis Report published by the National Association of Insurance Commissioners (NAIC) on an annual basis. The main health insurance relative combines this data with data from California as managed care plans in California report to a different regulator. The second retained earnings relative that covers long term care (LTC) and Medicare part D uses data from the NAIC Accident and Health Policy Experience Report.

CNSTAT report and recommendations

The BLS recently asked the National Academies of Science, Engineering, and Medicine, Committee on National Statistics (CNSTAT) for recommendations on improving the CPI, including recommendations on pricing health insurance. The final CNSTAT report was released in 2022.[3] CNSTAT recommended that the BLS continue to use the indirect method for pricing health insurance (recommendation 5.1) but made several recommendations for how the indirect method could be improved.

Smoothing

One issue with the pre-October 2023 method is there can be a lot of volatility in the retained earnings data from one year to the next. There is a question as to whether smoothing the retained earnings data using a moving average is desirable when calculating the relative. This section discusses the arguments for and against smoothing the annual retained earnings data.

The argument against smoothing is that the volatility represents real price changes that should be reflected in the index. If consumers on average have unexpectedly high utilization in a given year, they are receiving a benefit from having their premium locked in for the year. In terms of the insurance services, they are paying less for them (lower retained earnings) and getting more out of them (assuming the quantity of insurance services is proportional to utilization), which means that the price of insurance services has fallen. If this is considered a real price change, then it is irrelevant that it will likely be reversed in the following year. It can be viewed analogously to a sale, with consumers benefitting from prices that are lowered temporarily.

The argument for smoothing is that the relevant price when considering insurance is the ex-ante price.[4] Any ex-post deviations from expected utilization should not be considered real price changes. Individuals can be viewed as facing a fixed price schedule with uncertain utilization. The actual realized retained earnings to benefits ratio will depend on utilization and can show a change in price even if the price schedule is fixed. In similar situations where the price depends on total utilization, the CPI will hold utilization constant when pricing (for example, in the pricing of electricity). CNSTAT argued that the ex-ante price is the relevant price and suggested we consider smoothing (recommendation 5.3). We agree with CNSTAT that the ex-ante price is the more appropriate measure, so a relative calculated from smoothed retained earnings data will be a more accurate measure of price change. A limitation of smoothing is that if the retained earnings to benefit ratio changes for ex-ante reasons (reflecting a real ex-ante price change), smoothing will delay the impact of this change on the price index.

Incorporating retained earnings data sooner

Pre-October 2023, the annual retained earnings data is incorporated into the CPI starting in October after the calendar year for the retained earnings data. For example, in October 2022, retained earnings data was first incorporated into the index reflecting the change in the retained earnings to benefits ratio from 2020 to 2021. This annual change is smoothed over 12 months, so the 2021 retained earnings data will not be fully reflected in the index until September 2023.

Exploring the use of quarterly data to improve the timeliness of the index was another recommendation of the CNSTAT panel (recommendation 5.6).

Proposed changes to the CPI health insurance index

After conducting extensive research on these recommendations, we determined that the health insurance index could be improved by smoothing the retained earnings data and by using more timely, higher frequency data. In this section, we summarize how we plan to implement these changes to the methodology.

Smoothing the Retained Earnings Data

Following the recommendation to smooth the retained earnings data, we investigated different window lengths for the moving average and considered simple versus exponential moving averages. Ultimately, we chose to smooth using a 2-year simple moving average of the retained earnings ratio. Unusual deviations in the retained earnings are generally reversed the following year, so a 2-year average is sufficient for smoothing. Using additional years has less of an impact on smoothing and introduces unnecessary lag. We also favor using a simple moving average versus an exponential moving average as the exponential moving average will retain more of these 1-year deviations. The smoothing will be applied to both retained earnings calculations.

Semiannual updates

Overall, semiannual and quarterly updates are feasible and improve the timeliness of the index (by six months for semiannual updates and nine months for quarterly updates). A limitation of the quarterly updates is that the data is not provided at the level of detail that allows us to exclude out-of-scope plans. So out-of-scope plans are included in the calculation to impute quarterly changes in the in-scope retained earnings. The quarterly updating can increase volatility, and there is no way to know whether this volatility is driven by in-scope plans (reflecting a true price change that we would want to show in the index) or out-of-scope plans.

Updating twice a year is a clear improvement over the annual method and improves the timeliness of the index by six months compared to the annual updates. The additional benefit of improved timeliness (3 months) of updating quarterly is offset by an increase in volatility. At this time, we decided to switch to semiannual updates as it is not clear the added timeliness of updating quarterly is worth the increase in volatility. However, we will continue to research quarterly data and may incorporate it in the indexes at some point in the future. The semiannual updates will apply to the main retained earnings calculation. The second retained earnings calculation, covering LTC and Medicare part D, will continue to update annually in October, though we will continue to explore options for imputing the semiannual changes for this data.

Computation of semiannual updates

In terms of implementing the semiannual updates, the mid-year report includes data through June 30, and the final report includes the full year data. To calculate the 2nd half data, we subtract the mid-year report values from the full year data. Once we have the data by half, there are several options for creating semiannual relatives. The formula we chose to incorporate the semiannual updates is a sequential trailing 12 month relative of the retained earnings to benefit ratio. One issue is that the NAIC data are not complete and must be supplemented with data from managed care plans in California that report to a different regulator. The California data are not available at the necessary level of detail semiannually, so we impute the first half of California data using changes in the NAIC data.

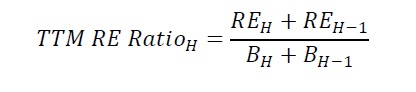

The trailing 12 month (TTM) index pools two halves of data and calculates the sequential relative. Once the second half of the year data is incorporated, the TTM and full year indexes will be identical. This is a desirable property of the TTM index as it will equal the full year index once each index incorporates the same data. For this reason, the TTM index is our preferred method as it will automatically correct any errors in the first half data, whether due to data reporting issues or imputation error relating to the California data. The main advantage of the semiannual index is that it will incorporate this change six months sooner than the annual index. The TTM retained earnings to benefit ratio in half H is:

The TTM sequential relative is:

Incorporating both changes, the TTM smoothed relative in half H is:

This is a semiannual relative, so the monthly retained earnings relative is calculated by taking the sixth root. The monthly retained earnings relative is:

The monthly retained earnings relative is multiplied by the relatives for medical benefits to form the health insurance relative. This is the calculation for the semiannual updates starting in April 2024 that will incorporate the first half of 2023 data. To switch from an unsmoothed annual index to a smoothed semiannual index, adjustments must be made to the October 2023 update that incorporates the 2022 annual data. We discuss the adjustments for this transition period in the next section.

Transition

Both methodological changes (smoothing retained earnings and incorporating retained earnings data sooner) introduce issues with the transition from pre-October 2023 methods. The first issue relates to the timing of the semiannual and annual indexes. Since, the semiannual index is six months ahead of the annual index, switching from annual to semiannual requires speeding up the next annual update. Instead of spreading the 2022 annual update over 12 months, it would be spread over six months by taking the sixth root instead of the twelfth root. Then, in April 2024, we would be able to update the indexes with 2023 first half retained earnings data since the 2022 data will be fully reflected in the index.

The second issue is that, unless a correction term is applied, switching from an unsmoothed to a smoothed relative will create a permanent distortion in the index. See the technical appendix on smoothing retained earnings for an example that illustrates how this distortion arises and how we derive the corrected relative.

Summary

Following recommendations from CNSTAT, starting in April 2024, we will switch the retained earnings calculation from an annual relative updated in October to a two year moving average using semiannual data and will update in April and October.[5] The next annual update in October 2023 will involve a six month transition to account for issues relating to changing in methodology. Table 1 provides a summary of the update timing moving forward.

Table 1: Summary of future updates to the CPI health insurance index Index Month Summary of update October 2023

Incorporate 2022 annual retained earnings data as an adjusted smoothed relative. For the main RE calculation, this update will be spread over six months. For the LTC/Part D calculation, it will be spread over a year. See the technical appendix for the derivation of the adjustment term. April 2024

Update the main RE calculation to incorporate the first half data for 2023. The update will be the semiannual sequential smoothed relative and smoothed over six months. The contribution of California managed care plans to the first half of 2023 retained earnings and benefits will be imputed from changes in the NAIC data. October 2024

Annual update to incorporate full year 2023 data. Second half of 2023 values are calculated by subtracting the first half totals (or first half imputed values for CA managed care plans). For the main RE calculation, the second half data is incorporated as the semiannual sequential TTM smoothed relative and smoothed over the following six months. For the LTC/part D retained earnings calculation, full year 2023 values are incorporated as a smoothed annual relative which is spread over the following 12 months. April/October

In future years, the April/October update process will continue. First half data will be incorporated in April and the full year update will occur in October. Note: This is the tentative schedule for the proposed methodology changes. BLS may amend this schedule in the future as we learn from experience.

Details regarding the transition to this new methodology are provided in: Technical Appendix to Improvements to the CPI Health Insurance Index: Transitioning from an unsmoothed to a smoothed relative

Last Modified Date: August 30, 2023

[1] For more detail on the CPI health insurance methodology see the CPI medical care factsheet.

[2] An alternative to the indirect method would be to price total premiums. Then, the prices and weights of medical goods and non-insurance services would only include out of pocket payments.

[3] The final report can be found here. Chapter 5 focuses on improvements to the medical indexes, with particular emphasis on the pricing of health insurance.

[4] The ex-ante price refers to the insurers setting premiums before knowing what the utilization will be during year. The premium is set based on expected utilization. The benefits spending we observe is based on actual utilization (ex-post), which may differ from what the insurance company expected when setting the premium.

[5] Part of the index will still use annual data but will also switch to using a two year moving average.

The BLS October 2023 CPI report is now available:

https://www.bls.gov/news.release/pdf/cpi.pdf

Go to its Table 2, Page 15 and scroll down to Medical care services. BLS claims the costs of Medical care services declined by 2% from October 2022 to October 2023. BLS claims the costs of Health insurance, the bottom item in the Medical care services section, declined by 34% from October 2022 to October 2023.

Get MHF Insights

News and tips for your healthcare freedom.

We never spam you. One-step unsubscribe.

Sponsors

Friends of MHF

")

Kirsten DeVries

Tom & Karen Nunheimer

Steve Ahonen

Ron & Faith Bosserman

Marlin & Kathy Klumpp

Sign Up for MHF Insights to keep up on the latest in Michigan Health Policy